Origionally published: August 22, 2025

Introducing the BLEC Ecosystem Report 2025

Over months of conversations, roundtables and surveys, our community has pooled real experiences: what’s working, what’s broken, and where we believe South Africa’s business ecosystem must go next. This 4-part article series previews the report’s biggest insights and sets out one simple idea: progress accelerates when we share a unified vision and build it with data. Consider this your guided tour of what’s happening on the ground, what could be better, and the practical ways we can pull together to move the needle.

Written by: Anza Kutama, BLEC Research Lead

Edited by: Tinashe Machokoto, BLEC Business Development Lead

Behind every successful startup lies a story of who believed in them first and why. In South Africa, the ‘who’ ranges from high-risk venture capitalists to patient development financiers and even international governments with strategic interests.

In this article, we discuss a key and fundamental function of business; financing. We’ve looked at some of the sources of venture funding in South Africa; VC funds, development institutions, and corporate venture arms, including international players like the US, China, and the EU. And we try to unravel how each of these entities in their categories determine who gets the money.

Venture Capital Funds

Compared to the other three sources of funding we’ll mention in this article, this is the one group that seeks pure profit from their deals with startups. Their return-centric model drives them to carefully evaluate startups not just on ideas, but on traction, scalability, leadership capability, and exit potential.

Oftentimes, and especially if the founding team sells a controlling stake in their company, VCs will play a hands-on role in shaping governance, growth strategy, and fundraising roadmaps. Some founders have expressed not only added pressure after accepting VC money, which is to be expected, but also a shift in the strategic direction of specs and development roadmaps of their products.

Founders would ideally want to accept funding from VCs that operate within the same industry as their company, as they are more likely to understand the market dynamics better, provide proper guidance, and procure helpful operational resources. On the flipside however, this can create the “We’ve been here before, we know better” dynamic that ultimately limits the powers of the founders and initial teams.

VCs that focus on a different industry or a multitude of industries are most likely interested in just the numbers, the financial performance – not product branding, company culture or niche product development details. Basically, anything that doesn’t tie back to revenue, margins, or a potential exit is less of a priority.

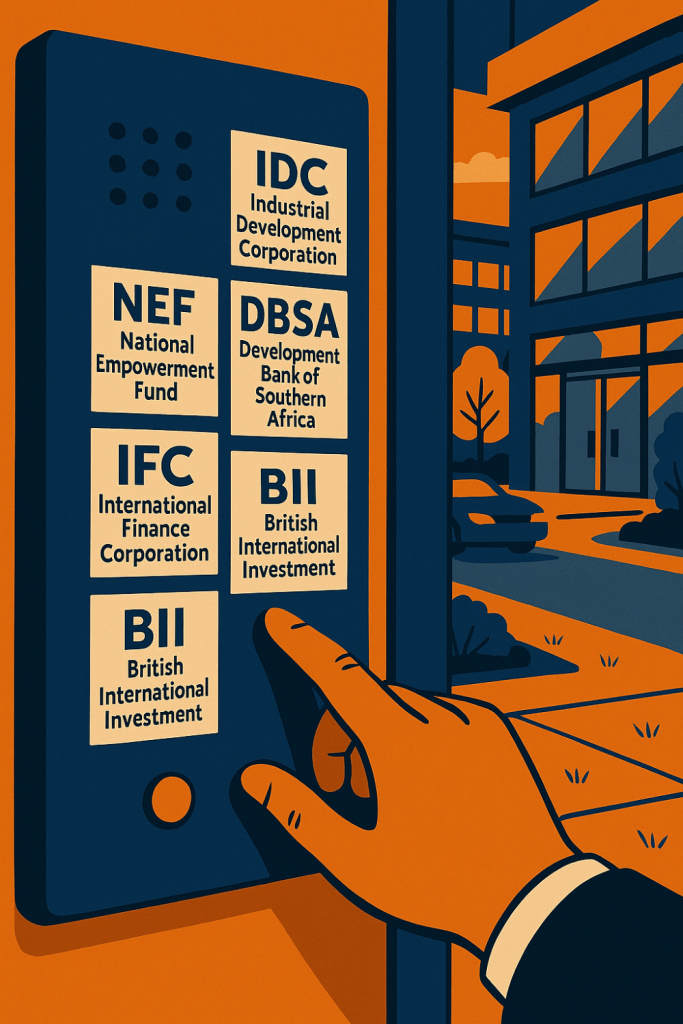

Development Finance Institutions (DFIs)

DFIs are often government-owned or multilateral entities that are meant to provide patient, long-term capital aimed at developmental impact instead of just profit. They’re more inclined to support systemic shifts and essential infrastructure through loans and equity.

South Africans DFIs include the Industrial Development Corporation (IDC), the National Empowerment Fund (NEF), and the Development Bank of Southern Africa (DBSA).

IDC is a state-owned DFI and provides funding for industrial and manufacturing sectors, innovation, and job creation. It’s often the entity that drives government programs such as the Presidential Employment Stimulus or the pursuit of Green Energy initiatives.

The NEF has a special focus on funding Black Economic Empowerment (BEE) and transformation initiatives. It provides equity and debt funding to black-owned businesses.

And last but not least, the DBSA, which is focused on infrastructure, regional integration, and sustainable development. By regional integration we’re referring to active efforts to align with institutions like AfcFTA and SADC where they would play a major role in financing, for example, renewable energy (e.g., as part of the Just Energy Transition framework).

You might often find these DFIs collaborating together on various financing initiatives. And as of February 2025, the NEF and IDC have entered into a corporate action for NEF to be the wholly-owned subsidiary of IDC. This decision is in line with government policy to consolidate South Africa’s development finance institutions given their often interconnected goals. Some of which include the June 2025 SA-H₂ Green Hydrogen Fund with DBSA, PIC (Public Investment Corporation), and international partners, namely Climate Fund Managers and Invest International.

International DFIs such as the two mentioned above also have a sizable footprint within the country. These include the International Finance Corporation (IFC) and British International Investment (BII) who allocate capital not just to these government programs but also to individual startups and venture platforms, shaping broader ecosystems.

In summary, DFIs act as catalytic investors, using their diligence and reputation to attract private capital, guide investment strategy, and de-risk early-stage markets such as certain renewable energies. If you’re a startup in manufacturing, IDC is your go-to. If you’re focused on transformative initiatives, the NEF has your back, and if you’re building physical infrastructure, the DBSA is available. And by this availability, we’re referring to the various programs across the country through which these institutions place their funds.

Corporate Venture Arms

Corporate funders invest strategically to monitor innovation, learn from emerging technologies, and potentially integrate promising solutions into their core operations. Their interest often lies in strategic alignment over pure financial return. This approach allows large firms to keep a finger on the pulse of high-potential startups, sometimes paving the way for eventual acquisitions, technology integration, or R&D collaboration.

Corporate venture arms, such as Alphacode Venture Partners by Rand Merchant Investment Holdings (RMI) or Vumela Enterprise Development Fund by FNB Business Banking and Edge Growth, don’t just provide capital. They keep a close eye on how nimble startups are building technologies, with the intention of integrating these innovations back into their portfolios or acquiring them outright. Sometimes they end up exiting the startups themselves to a better fitted buyer. These funds have provided capital for startups like Sweepsouth, Luno, Naked Insurance, and the Uber Driver Scheme.

Key takeaways

Unlike DFIs or corporate venture arms, VCs live and die by exits. Without a profitable sale, IPO, or merger, their fund cycle fails. This is why their lens is sharply tuned to leadership, scalability, and potential acquisition value.

International players arrive with a mix of diplomatic strategy and private capital ambitions. US, EU, and Chinese government-backed programs seek regional influence and partnerships, while private global VCs still see South Africa as a gateway market into the continent.

For founders, the challenge is not just in securing capital, but in matching the right kind of capital to their growth story. Whether that’s a VC with industry know-how, a DFI aligned with long-term transformation, or a corporate fund scouting for its next acquisition the key lies in knowing not all money is availed equally.

About the BLEC Report

The BLEC Ecosystem Report 2025 outlines key challenges and opportunities in South Africa’s business environment.

Download the full report here.

We encourage readers to get involved or contribute to the solutions presented here by reaching out here.